June 2026 update - Part 1

Hiab, Evolution Gaming, Teqnion, Diageo, Alphabet, Ashtead Technology, Booking Holdings, Judges Scientific, Nedap, Novo Nordisk and Wise.

It has been a long time, nearly six months, since I managed to pen a piece for Substack. I have been “working” quite a lot, although I don’t consider investing to be work in the traditional sense, given that researching companies is something I genuinely enjoy. In that sense, I will have a job for life, even if I am significantly lagging the index so far this year. Thankfully, my time horizon is measured in years, not months, so I won’t be firing myself and going passive, at least not yet.

Managing the demands of a young family is time-consuming, and as much as I may moan on occasion, I wouldn’t swap it for anything. Doing the accounts for a small business or trying to navigate the complexities of trust law constitutes “real” work, but hopefully, that part of 2026 is now largely behind me.

My initial plan was to write this as a single note; however, as it has grown in length, I will break it into two parts. Stage 1 will provide an update on the companies I have previously written about: Hiab, Evolution Gaming and Teqnion, as well as the new positions I opened in 2025: Diageo, Alphabet, Ashtead Technology, Booking Holdings, Judges Scientific, Nedap, Novo Nordisk, and Wise.

Stage 2, which I aim to publish next week, will cover the two new positions I have opened so far in 2026: Topicus and Copart. For reference, a typical new position for me starts at c1.5% of my book and is then increased or sold as I learn more.

Hiab (€54.50): A market leader across several industrial lifting niches (loader cranes, hook lifts, and tail lifts) with solid exposure to defense logistics. It is a capital-light, high-return business; see my earlier Substack pieces for more detail. Since January, the shares are up slightly, although they have traded within a wide range (€40–€60). Operationally, the outlook for Hiab is improving, with order volumes typically lagging behind the major truck manufacturers, most of which have seen significant pick-ups in orders, particularly in North America (see Daimler Truck’s Q1 results). Hiab’s defense logistics business should also begin to contribute more meaningfully.

The main news at Hiab in the last six months, however, has been the announcement of a relatively large acquisition: Labrie, the number-three player in the North American waste and recycling truck market and the leader in the fastest-growing segment, automated side loaders. Hiab had been focused on smaller bolt-on deals, so at €890 million (against a Hiab market cap of €3.5 billion and an EV of €3.25 billion), this acquisition is a larger strategic move.

On the face of it, the deal looks attractive: Hiab has been following Labrie for five years, the business is not a turnaround (it boasts higher margins than Hiab at c17% EBIT), and it was purchased at an attractive 9.2x EBITDA multiple before synergies. It will be financed with cash and debt at a cost of 3.6%. The transaction will move Hiab from a net cash position to a net debt/EBITDA ratio of just over 2x, but given Hiab’s cash generation, I expect them to deleverage relatively quickly. The deal is significantly accretive c18% pre-PPA.

What’s not to like? My primary concern is that Hiab is buying Labrie from private equity; the chances of securing a “bargain” from a PE firm are rarely high, which raises a red flag. It hasn’t been enough to trigger a change in my position yet, as I like the current setup at Hiab. I see a clear reason for the order book to improve significantly in the second half of 2026 (and possibly Q2 2026), following the higher order volumes seen at the main truck manufacturers. Hiab gave little away at the Q2 pre-close call.

On my numbers, which assume Labrie is not consolidated until the start of 2027 (though it will likely be earlier, with an estimated close in Q3 2026) Hiab trades at 20x PE for 2026 and 15.6x for 2027 including PPA (13.9x excluding PPA). Upside to these figures will likely come from a recovery in equipment orders. At the moment, I am assuming only a very slight organic growth recovery of 2% in 2026 and 5% in 2027, which, given the leading indicators mentioned earlier, seems conservative. This rating for a business of this quality also feels modest. For now, it remains a top-10 position for me.

More detailed piece on Hiab business:

https://substack.com/@tci77/p-161011525

Evolution Gaming (SEK 700): The B2B leader in online gaming. Year-to-date, the shares are up 12%, but they remain significantly down over the three- and five-year periods and are still in a 56% drawdown from their peak. In January, I wrote that the stock was pricing in a very negative scenario. In February, following the FY 2025 results, sentiment worsened, and at SEK 557, I added to my position—primarily to bring it back to a 3% weighting and keep it in the top 15 of my fund (my overall average price is cSEK 900, so no victory laps here).

Growth rates at Evolution have slowed significantly, and the headwinds are well-known: European ring-fencing and channelization pushing gamblers to non-regulated sites, and the persistent issue of Asian cybercrime. For Q4 2025 and Q1 2026, FX was also a major headwind; reported sales in Q1 2026 were down 1.5%, while constant currency growth was c7% YoY. Personally, I found this to be a positive, suggesting the business is not in structural decline, whereas it felt like many investors focused only on the headline figure.

Evolution also announced on March 18th that it would not be paying a dividend in 2026. Strangely, the announcement of a €2 billion buyback did not arrive until May 18th, a date well after both the Q1 2026 results and the AGM. Management had hinted at a buyback, but I have no idea why it took two months to properly communicate the policy; I have consistently found Evolution’s investor relations department to be subpar or, at best, unresponsive, and this was unfortunately another example.

Putting aside personal frustrations, the decision to cancel the dividend (c€570 million) in favour of a €2 billion share buyback should be applauded. With a market cap of c. €13 billion, the €2 billion allocation allows them, all else being equal to buy back c. 15% of outstanding shares. What is also clear is that at the current price, they are in a hurry; since the buyback started less than a month ago, they have already acquired c1.5% of outstanding shares. Furthermore, if the founder shareholders and Kenneth Dart (who hold a combined 40% of the company) do not sell, Evolution is effectively buying back 25% of the free float. Logically, this should place a firm floor under the share price.

It should also be noted that a €2 billion buyback does not put the balance sheet under major pressure. Evolution had net cash of €1.2 billion and generates around €250 million of cash per quarter. If the share price remains stagnant, they will likely be very aggressive; there is a chance they briefly enter a net debt position, but this would be cleared very quickly given the business’s cash generation. If, like me, you do not believe the business is structurally broken and expect most headwinds to pass, the share buyback is clearly compelling.

At today’s price, Evolution is valued at 11.3x PE (I am 6% ahead of consensus on EPS, mainly due to the lower share count), 9.3x EV/EBIT, and an 8.3% FCF yield. In conclusion, I would frame Evolution as being lowly rated, with knowledgeable insiders buying aggressively—with €1.8 billion left to purchase—explicitly stating that they believe the market is mispricing the stock. This provides a degree of downside protection and an interesting option if the underlying business pivots back to growth. It is worth highlighting that in Q1 2026, the North American business grew by 10% (in Euros) and LatAm grew by 29% (in Euros). In addition, the comps for the European business (down 12% in Q1) start to get easier now that they are lapping the ring-fencing measures. A mid-single-digit growth rate is very plausible and could justify a decent re-rating. On the downside, one thing that would cause me to exit would be if insiders began actively selling into their own share buyback. A future threat I am also considering is whether AI could eventually allow online operators to do away with physical studios and live tables; this would clearly be a significant threat to Evolution’s business model. I have attached an interesting article on this topic below.

https://next.io/news/features/is-the-robot-apocalypse-coming-for-live-casino/

Also attached is a good review on Evolution by Maxx Waring:

And a detailed review of the Q1 2026 results by Ali Gunduz and his Do Not Distribute substack:

Diageo (£15.30): Owning Diageo has certainly increased my alcohol consumption, and they haven’t been celebratory drinks. Year-to-date, the stock is down 5%. In January, I noted that I saw a risk to consensus numbers given the “mood music” coming out of the company, and with the arrival of a new CEO, there was always the potential for a “kitchen sinking” of the financials or a dividend cut. That has largely played out: the dividend was effectively halved, and there was a slight downgrade to FY26 guidance for both sales and operating profit, though free cash flow was maintained.

What we are still waiting for is the full strategic review by new CEO Sir Dave Lewis, which will arrive alongside the FY 2026 results at the start of August. A margin reset is possible, and to an extent expected—but looking at consensus estimates for 2027 and 2028, it does not appear to be fully reflected yet. I don’t mind the dividend cut; combined with the sale of East African Breweries and the Indian cricket team (via United Spirits, in which Diageo owns a 56% stake), these moves should help leverage move toward a more comfortable level.

What attracted me to Diageo in the first place were its world-class brands, its nature as a long-duration asset, and an attractive valuation. The assets remain unchanged, and the valuation has arguably become more appealing, with the stock trading at a free cash flow (FCF) yield of c7%. For now, I have maintained my position rather than adding to it, as I am waiting for the CEO to fully take ownership of the strategy; the “kitchen sink” could still make an appearance on August 6th.

Very good write-up on Diageo as part of a wider piece by Sector Stories substack:

Teqnion (SEK 159): Since I last wrote about Teqnion in January, not a huge amount has changed; the share price is down slightly, and I have come to the same conclusion, arguably with more confidence. The Q4 2025 results were “okay” but slightly disappointing compared to the strong Q3 results; part of this was due to timing, a view supported by the Q1 2026 performance. On my updated numbers, Teqnion trades at 16x 2026 earnings (13.3x 2027).

Crucially, the business has clearly turned the corner following a tough 2024 and H1 2025; the last three quarters support this. I expect earnings to increase by c70% in 2026 (+20% in 2027), and I believe the improved operational momentum will eventually trigger a re-rating, especially given that larger serial acquirers trade at roughly double Teqnion’s current multiple.

I have been adding to my position over the last week, and it remains one of my largest holdings. I like the setup: improving operational momentum, the public-to-private multiple arbitrage, the low rating versus peers, and a management team that is genuinely frank about the issues they have faced. There aren’t many CEOs who would grade their own performance in an annual report as an “F” for 2024 and a “D-” for 2025. The point is that Teqnion is moving toward a more “normal” operating performance for its existing businesses, and the runway for highly accretive acquisitions remains long. For the stock to work, I don’t need the CEO to hit an “A” just a “C” or a “B” and given his track record since founding the company in 2006, I don’t think that is overly optimistic.

For more background detail on Teqnion and what the actual business is, have a look at a substack piece written by slow compounding, this provides an excellent deep dive.

It is also worth listening to some interviews with Daniel Zhang of Teqnion to get a better feel of how the two key people in Teqnion operate, below is a link from the Dutch investors podcast:

https://tdi-terminal.com/dashboard/library/96c1d6f4-31bb-4b75-b726-8ec187cbe522

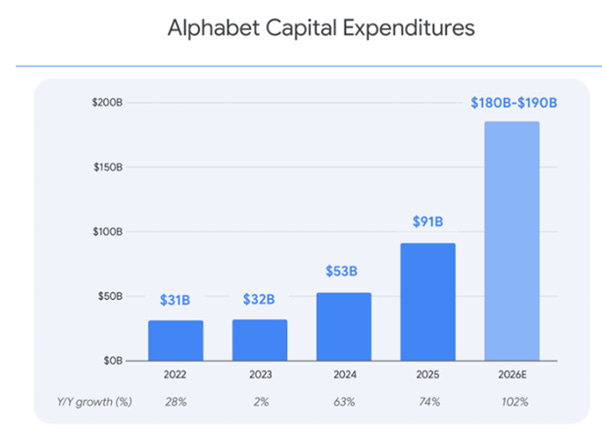

Alphabet ($360): The shares are up 14% YTD. I have very little value to add on the name; I have included it here only for the sake of consistency and completeness. In January, I noted that my position was under review, and that remains the case. The valuation is no longer particularly interesting, and the recent announcement that they are issuing $80 billion in equity—while helping to fund their massive AI ambitions, the fact that they are issuing equity at these levels isn’t the greatest signal. Clearly, capital expenditure commitments will continue to ramp from already extraordinary levels, with 2026 guidance now at $180–$190 billion and expectations for a “significant increase” in 2027. The central question remains what returns they will ultimately generate on this capital. So why am I still sitting on my holding? In simple terms, it acts as a partial hedge against some of my other positions regarding potential AI-driven disruption, and I still believe its portfolio of businesses occupies an enviable strategic position.

Below is a link to the excellent Andrew Walkers blog on Google’s equity raise, which provides interesting commentary and analysis over 3 parts. The link below is to part 3, but links to part 1 & 2 can be easily found.

Ashtead Technology (£4.52): An oil & gas and offshore wind equipment rental business. Year-to-date, the stock is up strongly (c50%). Ashtead has clearly benefited from a shift in narrative, partly driven by conflict in the Middle East. A higher oil price is supportive of offshore projects, while the renewed focus on energy security aids Ashtead in the geographic markets where it operates (for both oil & gas and offshore renewables). Interestingly, Ashtead is no longer one of the most shorted stocks in the UK; at the end of 2025, short interest was c. 9%, but it has since fallen to c. 1.1%, and this covering has clearly been a factor in the strong year-to-date performance. Consensus numbers do not appear particularly aggressive, factoring in mid-single-digit top-line growth and slight margin compression from the elevated levels seen in 2025. This results in an EPS of c. 47p, a P/E of roughly 9.6x, and an FCF yield of c. 7% (though this is not adjusted for a fair amount of growth capex). The balance sheet remains solid, with leverage at just over 1x EBITDA, and the business has a strong track record of executing accretive bolt-on acquisitions. I haven’t changed my position YTD and am happy to maintain it at c. 1.7%.

For a more detailed write-up see the Rock & Turner substack link below.

Booking Holdings ($172 or $4300 pre-split): The leading online travel agent; it’s an excellent, high-return, cash-generative business. In January, I noted that I had just started a small position, writing: “The reason I am building a position gradually is that even though the business is performing excellently operationally, I wouldn’t be surprised if there was a wobble with market sentiment around the narrative, specifically the potential threat from AI agents. Clearly, software names have been very beaten up on the back of AI and vibe coding, and it is quite possible that online travel agencies could see a narrative of increased AI agent threats.”

It is fair to say that this narrative took effect, and Booking did sell off on the fear of AI and how it might impact their business. In addition, the war in the Middle East also hasn’t been helpful, given that it acts as a major travel hub, especially when combined with the secondary impact of higher energy/fuel costs and squeezed consumers. As a result, Booking is down 19% YTD, and it has provided me the opportunity to take a position of over 2%; my average price is now $173.5 (or $4338 pre-split).

The AI agentic threat, in terms of narrative at least, reduced on March 5th when ChatGPT announced that it wouldn’t be completing purchases within the app and would instead be directing users to third-party apps such as Booking. In this case, AI just becomes another funnel, just like traditional search, and is precisely why Booking spends over $7bn pa on digital advertising. My view remains that AI is more of a tailwind than a headwind for Booking, and my view on the stock remains the same. Booking provides users with trust; I know that if I use Booking, I have a lot of protection if something goes wrong. Secondly, Booking has a lot of stickiness from its loyalty plans, with over 50% of room nights coming from the higher tiers of the Genius loyalty scheme. Thirdly, Booking has an amazing set of data (demand and supply) and knowledge about its customers and providers, so there is a reasonable chance that they can build a leading AI agent within their own app. Fourthly Booking provides genuine value for its hotel and alternative accommodation suppliers.

The impact from the war in the Middle East is a headwind to the business, and this was partly seen with the Q1 results, with March seeing a spike in travel cancellations knocking 2% off gross bookings and room nights. The FY 2026 guidance was also slightly downgraded, with gross bookings now forecast at high-single-digit to low-double-digit growth (down from low-double-digit), and FY EPS now guided at low-mid teens growth (down from mid-teen growth, assuming the war in the Middle East lasts for the 2Q only). Given the headwind, I find this guidance incredibly resilient. What was also very interesting in Q1 was that Booking bought back $3.6bn of stock (c2.7%), which was slightly above the $3.1bn of FCF they generated in Q1. The $3.6bn was the largest single-quarter share buyback in the company’s history. The business is highly cash generative, and at the current valuation, the board clearly believes the opportunity lies in using as much free cash flow as possible to retire equity. On my numbers, the stock is trading on a FCF yield of 6.9% for 2026 and a PE of c17x. One potential risk to bear in mind is the threat of fines within the EU, the timing of which is difficult to know.

In summary, Booking Holdings is a high-quality business at an attractive price, exposed to a structural long-term growth trend of increased travel. The AI narrative threat, I believe, is overdone, and the recent headwinds of war in the Middle East will eventually pass. In the meantime, the company is cannibalizing itself with large share buybacks.

Good piece on Booking Holdings from Daniels Deep Dives:

Judges Scientific (£49): A UK serial acquirer focused on niche scientific equipment. YTD the stock is down 15%. News on Judges has been relatively quiet, with no new acquisitions, a trading update in January, and then the release of the FY 2025 results at the end of March. As expected, the 2H of 2025 was weak, with the main lowlight for FY 2025 being N American orders -23% (US academic spend). Guidance for FY 26 is for an EPS £2-£2.50 (peak in 2023 at £3.69, and £2.75 in 2025). The guidance for FY26 assumes no recovery in US academic spend (this feels conservative, with the main risk being timing of grants); it also assumes no Coring expedition (more likely start of 2027). For 2026, the guidance feels derisked, with upside potential from a quicker recovery in US academic spending, an earlier Coring expedition, or M&A. The balance sheet is solid at 1.5x ND/EBITDA; given they have historically acquired businesses at 4-5x EBITA, any deal is likely to be taken well. My view on Judges hasn’t changed; the valuation is attractive with a FCF yield >5%, the long-term track record of capital allocation is excellent, and the headwinds, in my opinion, are well known and temporary. Given the weak performance, I have been adding to my position to maintain it at its original size. My average in price is now c£61.5.

Review by Chris Waller post the FY 2025 results that were released in March.

A good write-up from post anchor stocks on the FY 2025 results.

Nedap (€97): A small Dutch software and hardware provider focusing on four main areas: livestock management (”Fitbit for cattle”), healthcare, retail (loss prevention & inventory management), and security (access control). YTD the stock is +5.8% (and a c4% dividend on top). Operational performance has been good, with the FY 25 results published at the end of February showing 11% top-line growth, and EPS +32% to €3.72. The Q1 trading update (sales only) confirmed that the company continues to generate positive momentum with revenue +14.3% (and recurring +15.5%); this should likely translate into good operating leverage. The balance sheet is strong with virtually zero net debt. The CEO stepped down for health reasons in April and was replaced by the COO, who has been with Nedap since 2004 (so expect business as usual). Nedap has generally continued to avoid any major AI narrative threat to its software business—this might be because it is small and not widely followed. On 2026 estimates, Nedap could do c€30m of FCF, which would place it on a FCF yield of 4.7%, which clearly isn’t unreasonable. I did reduce my position at the end of 2025, and it is down to 1% of my book. For now, I will continue to follow the company and maintain the position, although I have been considering switching the position entirely into Topicus and Booking Holdings.

Novo Nordisk (DKK 295): YTD the stock is down c. 11%. Having bounced strongly in January, Novo continued its trajectory down following the release of the FY 2025 results and, more importantly, the guidance for 2026. The 2026 guidance was clearly disappointing, with sales and operating profit forecast to decline -5% to -13%, despite a strong initial launch of the Wegovy pill. Given that guidance in 2025 was a bit of a disaster, you could make a reasonable argument that management is being particularly conservative. At the Q1 results, guidance was technically increased, but if you blinked, you missed it. The new guidance for 2026 is for sales and operating profit to decline -4% to -12%. The increase was mainly symbolic—in my opinion, a case of management wanting to show something positive while remaining conservative. The guidance was also made just a few weeks after Lilly’s competing weight-loss pill had launched, so again, you can imagine a strong argument for why management would want to remain cautious.

The positive news is that the Wegovy pill continues to perform very strongly in the US, and the launch of Lilly’s Foundayo pill hasn’t really had an impact (yet). For 2026, I think it is highly likely that Novo will upgrade guidance because of the Wegovy pill. A second positive is that the FDA is taking more steps to crack down on compounding; on the 30th of April, the FDA proposed removing three GLP-1s from the 503B bulks list. The review ends June 29th; if the FDA finalizes this rule, it will significantly reduce the availability of GLP-1s from compounders. Realistically, this won’t happen until mid-2027. There were an estimated 1.5m people in the US taking unapproved GLP-1s, and these have been linked to over 1150 adverse events, 100 hospitalizations, and 10 deaths, all of which increases pressure on the authorities to act. This could potentially act as a decent tailwind for 2027.

On the negative side, Novo scored something of an own goal in February with the REDEFINE IV trial results. These showed that its next-generation product, CagriSema—a GLP-1 and amylin combination expected to be approved by the end of 2026—was inferior to Zepbound on overall weight loss (23% versus 25%). This raises questions about CagriSema’s sales potential, although it would still be the first GLP-1 and amylin combination product on the market. The other main concern is Lilly’s strong obesity-drug pipeline, particularly retatrutide, a triple agonist that has delivered strong results and is likely to reach the market in 2027. Novo also has a triple agonist in development with promising early data, but its earliest launch would be in Asia in 2028, and probably not until 2029 or 2030 in the US.

As a simplistic generalist, what I keep coming back to is that the obesity market is huge, and we are at the beginning of the market penetration. The market is also heterogeneous, and I currently don’t believe there will be a “winner-takes-all” product; not everybody will want a 25% weight loss, or an injection, or certain side effects. For this reason, I intuitively don’t currently believe Novo is ex-growth. Pricing in 2026 and 2027 is likely to be a significant headwind, but with the success of the Wegovy pill, I can see a route to growth. The brand, weight loss, and fewer drug interactions make it appear superior to me versus Lilly’s Foundayo, yet expectations seem lower, possibly since Lilly has been so successful with Mounjaro/Zepbound. The current valuation suggests this isn’t the case. Novo also has some interesting products in the pipeline outside of obesity.

When looking at the valuation of Novo, you need to consider that it has been going through a huge investment phase over the last few years, with capex-to-sales c. 20% (in theory, this physical production capacity and manufacturing know-how should provide a certain barrier to entry). For 2027, I would expect capex of c. 10% of sales, which remains elevated versus Novo’s historical levels and against industry standards of 5–7%. Dropping capex to c. 10% of sales results in cash generation at Novo significantly increasing, and at today’s valuation, would see Novo on a c. 7% FCF yield. At this valuation, I see an interesting risk-reward, although given the dynamic nature of the obesity drug market, I will limit myself to a 1.5% position.

Wise (£8.40): A fast-growing fintech with a focus on lowering the cost of cross-border transfers and sharing those lower costs with customers to drive further growth, a very powerful flywheel. The preliminary FY 2026 results released in April showed strong operating momentum, with active customers up 21% YoY and a 25% increase in cross-border volumes. The full release is on June 25th. On May 11th, the company moved its primary listing from the UK to the US; so far, it clearly hasn’t led to a re-rating!

When I first wrote about Wise in January, I highlighted two main risks: “1) Regulatory: there is always the chance of a money laundering or financing of terrorism tail-risk event.“ On June 1st, the story broke that Wise was being investigated by Belgian authorities regarding money laundering. The probe was initiated after Wise Europe’s accounts were identified in “hundreds of criminal files” and cross-border assistance requests from over 30 European countries. It seems even money launderers are cost, and time sensitive. I don’t wish to downplay it, but these investigations are relatively common. There is clearly potential for a fine or forced remedial actions, both of which could be costly, although, looking at past fines within the sector, they haven’t tended to be too onerous. Given the uncertainty and the increased risk, the shares fell on this news.

The second risk: “2) Wise is exposed to falling interest rates since this reduces the income they earn on customer balances. So, falling rates are a headwind, but the growth rates that Wise is currently achieving in customer balances are going a long way to offsetting this.” On this front, the interest rate environment has clearly changed due to the US/Iran conflict. The ECB raised rates last week by 25bps, and expectations are now for the Fed to increase rates rather than cut. A rising-rate environment acts as a tailwind for Wise. Although I wouldn’t count these risk factors as a 1-1 draw, given the uncertainty created by the money laundering investigation, I would currently call it a 2:1 loss.

Despite the money laundering risk, I still really like Wise, and I have slightly added to my position to maintain its size. The valuation remains attractive; at current levels, the stock is trading on an (adjusted) FCF yield of 5.7%. Given the growth and the very long runway, this seems quite compelling. Wise also sits on £1.3bn of net corporate cash and is highly cash-generative and asset-light. I expect that on June 25th, they will announce a large share buyback.

If you have more interest in Wise, I suggest you read one of the following notes. There have been some excellent pieces published on Substack.

Very in-depth piece by Rock & Turner – June 9th

A piece by compound with Rene – 21st May

Review of business by Fiscal.ai

Disclaimer: This is not investment advice, do your own research, all views expressed are my own. I may have a position in the company mentioned and I may increase or sell my position without providing any notifications